Retirement planning : Financial freedom

In today's fast moving world, the word Retirement has changed. Now people call it FINANCIAL FREEDOM. No one wants to work till 55 or 60. They want to earn quick and retire quick to live the life they want. But is it possible without proper planning and execution?

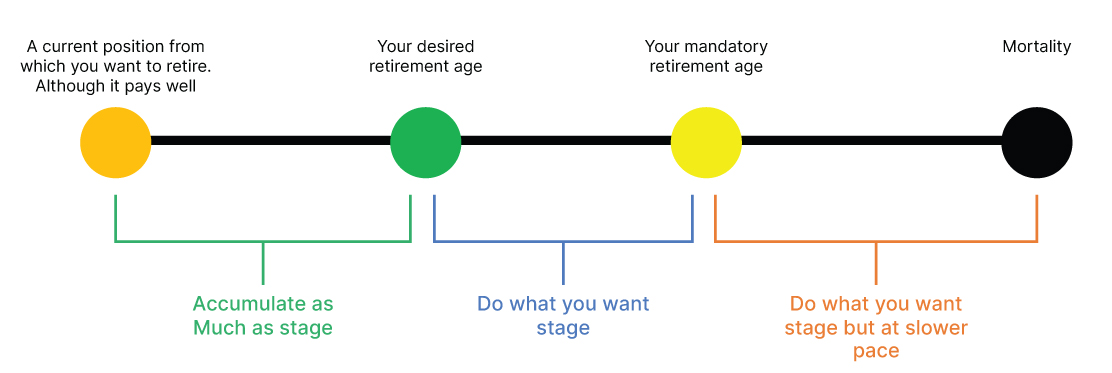

Planning towards your retirement can no longer take a back seat.

Retire with dignity, sounds great in itself. Ensure that the time when you retire you should be liable in carrying enough funds, which prospers in meeting with your expenses by maintaining the same established life style. Right Fulfillment curve: survive, comforts, Luxury, Enough, Life purpose, peace of mind & financial freedom.

How crucial is retirement planning for you? What time appears to be best for you to invest? How planning in advance turns out to be fruitful for your coming years? Our experts can help you with the best solutions to the above questions and any others that may be of concern to you

Choose excellent retirement planning services from us and let your money grow for your previous retirement years.